February 8, 2022

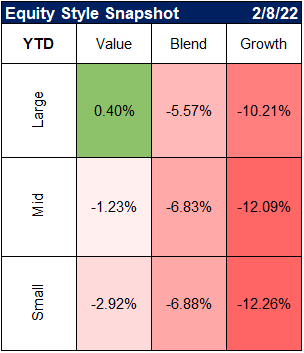

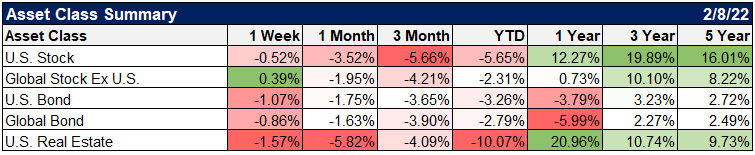

Market Performance (YTD)

Source: YCharts

Disclaimer: Past performance is no guarantee of future performance

The wild ride continues

what a week

– today was the worst day for Nasdaq 100 since September 2020

– Monday was the best day since March 2021 pic.twitter.com/IlpVvJqh6G— Katie Greifeld (@kgreifeld) February 3, 2022

Disparate corporate earnings was a driver of riotous increase in single-day S&P 500 stock dispersion in Feb; weighted std dev among single S&P 500 constituent daily returns shot up to 65% annualized last Thurs, highest single-day reading since Nov 2020

@SPDJIndices pic.twitter.com/QoeQSaf88I— Liz Ann Sonders (@LizAnnSonders) February 7, 2022

Especially for some of the big tech stocks who reported earnings

*META FALLS 25%, SET FOR BIGGEST VALUE WIPEOUT IN MARKET HISTORY$FB

— *Walter Bloomberg (@DeItaone) February 3, 2022

Largest market cap decline ever, by a lot pic.twitter.com/p4Exz9AK5h

— Michael Batnick (@michaelbatnick) February 3, 2022

— Brian Cheung (@bcheungz) February 3, 2022

And hawkish central banks remain central to the story

US rate hike expectations just keep going up

Market Expectations for Fed Rate Hikes: (up,up,up) pic.twitter.com/Sp3RlvfX5K

— Michael McDonough (@M_McDonough) February 4, 2022

The ECB also becoming unexpectedly more hawkish

🇪🇺 Major hawkish change as the ECB no longer expects inflation "to decline in the course of [this] year". This sentence was removed from the inflation assessment section. Risks "tilted to the upside, particularly [but not only] in the near-term".

— Frederik Ducrozet (@fwred) February 3, 2022

"The European rates market has shifted fast – in only early December the German 10-year bund yield was -40bp… Our rates strategists have just upgraded their YE forecast and now expect the 10-year Bund yield to reach +50bp in 4Q 2022"

— Jonathan Ferro (@FerroTV) February 8, 2022

And the US jobs report blew out expectations, likely only furthering reasons for the Fed to be hawkish

BOOOM. Jobs report crushes expectations.

467K new jobs in January vs. expectatiosn of 125K. So much for the big Omicron jump.

The unemployment rate rose to 4%, however, this is in the context of a big LFPR jump.

Also HUGE upward revision to last month.

— Joe Weisenthal (@TheStalwart) February 4, 2022

The big takeaway from the jobs report = The US jobs market is even stronger than we thought.

+476,000 jobs added in January

+510,000 jobs added in Dec. (prior estimate was 199k)

+647,000 jobs added in Nov. (prior estimate was 249k)https://t.co/tfSauSW55K pic.twitter.com/ZA2WmY3j43— Heather Long (@byHeatherLong) February 4, 2022

So where do we go from here?

There are a couple different viewpoints..

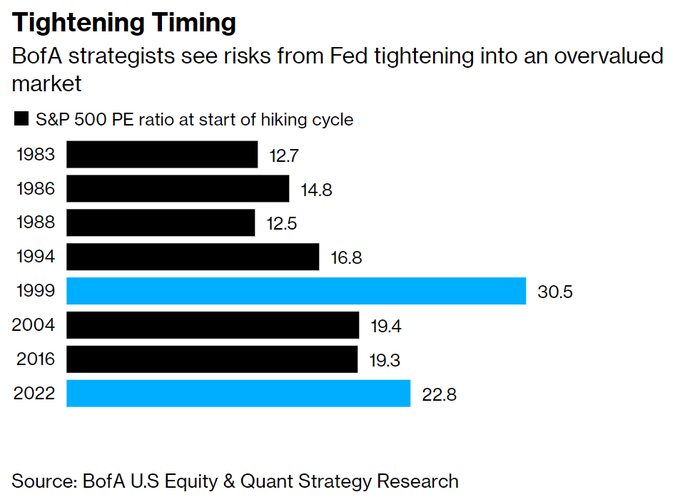

"Fed is unlikely to keep moving further and further into hawkish territory, at least relative to what is priced in currently"

☝️JPM v BofA 👇

"Fed hiking into an overvalued market… market is more expensive ahead of tightening than in prior periods, with the exception of 1999"

— Jonathan Ferro (@FerroTV) February 7, 2022

BofA is expecting 7 hikes (!) but also candid about their past hike forecasts..

The funny thing about this chart that went around last week is that no one mentioned how the market keeps UNDERestimating how much the Fed hikes once the hiking cycle starts and the same when cuts come in – BofA's insane call for 7 this year notwithstanding. pic.twitter.com/a6vVW3XBWr

— 𝐄𝐟𝐟𝐢𝐜𝐢𝐞𝐧𝐭 𝐌𝐚𝐫𝐤𝐞𝐭 𝐇𝐲𝐩𝐞 (@EffMktHype) February 7, 2022

And here are two good visuals explaining why rate hikes are scaring certain parts of the market

One chart to demonstrate why tech and rate hikes don't mix well.

Higher rates eat away at the value of a dollar over time.

Many companies trade on current or (close) future earnings. Red circle.

Many younger tech cos trade on far out earnings potential. Blue circle. pic.twitter.com/NiDcn1Ov1i

— Callie Cox (@callieabost) February 7, 2022

But widening credit spreads, falling inflation expectations, slowing earnings, and declining PMIs argue the fed will come nowhere near 7 rate hikes

Somethings different this time. Last year, when yields were pushing higher, credit was well behaved and credit spreads remained thing. This time, spreads are widening — often a canary in the coal mine for a more disorderly sell off pic.twitter.com/PfmEjb7Npf

— Dani Burger (@daniburgz) February 8, 2022

1yr inflation expectations now dropping waaaay below economist consensus (>1 ppts divergence)

Remember that central banks rely on economist projections. They will have to scale down inflation forecasts big time in H2-2022 pic.twitter.com/BJXX7KFNIZ

— AndreasStenoLarsen (@AndreasSteno) February 7, 2022

Earnings surprise in the US remains high. However, the key so far is guidance, as good earnings were discounted. And guidance so far is mostly weak.

via Bloomberg pic.twitter.com/LxZZ1i4WCW

— Daniel Lacalle (@dlacalle_IA) February 7, 2022

Forward earnings estimates are trending weaker than prior COVID quarters pic.twitter.com/utQAk8cjAL

— Mike Zaccardi, CFA, CMT (@MikeZaccardi) February 7, 2022

Earnings season is coming along, and so far 169 companies have reported, with 77% beating estimates by an average of 5%. For me, the key metric is the estimate for 2022, which at 7.9% has already come down a full percentage point from the start of the year. pic.twitter.com/GnJsYdqGxs

— Jurrien Timmer (@TimmerFidelity) February 4, 2022

Another 🔥 research note from @MichaelKantro on the unfolding #macro backdrop & treasury yields. Usually #PMIs are ↗️ during a #Fed tightening cycle, but PMIs are likely go ↘️ over '22.

"Long-term bond yield rarely rise when PMIs are falling even during Fed rate hikes." 🤔 pic.twitter.com/hCf5lqJZyf

— Matthew Miskin, CFA (@matthew_miskin) February 7, 2022

Charts Of The Week

If $BABA was part of the S&P 500 Value Index, it would be in bottom 25 percentile.

Kroger, CVS Health and Kraft Heinz are trading at higher multiples than Alibaba. pic.twitter.com/SJNLSnUVdR

— David Ingles (@DavidInglesTV) February 8, 2022

I wondered when Amazon would start disclosing advertising revenue. Answer: $31bn in 2021 – roughly the same size as the entire global newspaper industry.

AWS produced $18.5bn operating income – it's plausible that the ad business is now more profitable. pic.twitter.com/MCq3zjp3Kc— Benedict Evans (@benedictevans) February 3, 2022

Back in 2009 the U.S. had an excess of 1.9 million vacant housing units. As of the fourth quarter of 2021 there was an undersupply of 1.8 million vacant units. pic.twitter.com/RwKteSoIzt

— 📈 Len Kiefer 📊 (@lenkiefer) February 2, 2022

Global food prices are near the record high reached in 2011, as per a UN index: pic.twitter.com/am620o7NwF

— Lisa Abramowicz (@lisaabramowicz1) February 3, 2022

“The financial crisis taught corporates and consumers about the risks of leverage and the unsustainable leverage that we saw during the financial crisis is nonexistent today and bloated leverage ratios post-recessions are non-existent today.” – BofA pic.twitter.com/X0rPR8WoVq

— Sam Ro 📈 (@SamRo) February 7, 2022

This chart from today’s @FT on the growth in pre-tax #earnings illustrates the massive increase in income inequality in the US since 1976. This is part of the notable worsening in the #inequality trifecta — of income, wealth and inequality. #economy pic.twitter.com/v899i2Dle0

— Mohamed A. El-Erian (@elerianm) February 8, 2022

US Real average hourly earnings YoY pic.twitter.com/5YNXed4NdM

— 🅰🅻🅴🆂🆂🅸🅾 (@AlessioUrban) February 4, 2022

Disclosure

Clear Rock Advisors, LLC is registered with the SEC as a registered investment advisor with offices in Texas. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Clear Rock Advisors, LLC) or any investment-related or financial planning consulting services will be profitable, equal any corresponding indicated historical performance level(s), or prove successful. It remains the client’s responsibility to advise Clear Rock Advisors, LLC, in writing, if there are any changes in the client’s personal/financial situation or investment objectives for the purpose of reviewing, evaluating or revising Clear Rock Advisors, LLC’s previous recommendations and/or services, or if the client would like to impose, add to, or modify any reasonable restrictions to Clear Rock Advisors, LLC’s services. A copy of Clear Rock Advisors, LLC’s current written disclosure statement discussing its advisory services and fees are available upon request.