August 24, 2023

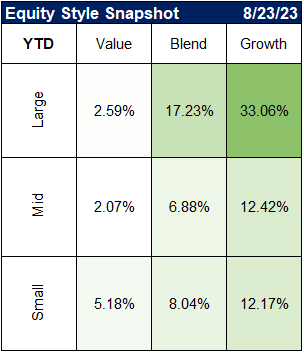

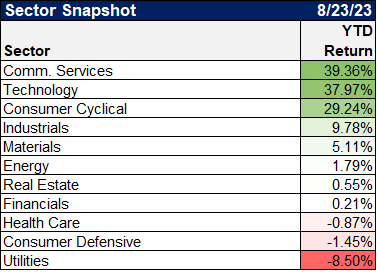

Market Performance (YTD)

Source: YCharts

Disclaimer: Past performance is no guarantee of future performance

BREAKING: Atlanta Fed's GDPNow Index soars to 5.03% pic.twitter.com/ssPnrKJC1Q

— Robert Burgess (@BobOnMarkets) August 15, 2023

What a monthly mortgage payment would look like for a new home buyer in the US, based on the median existing home price and the average 30Y fixed-rate mortgage, assuming a 20% down payment: pic.twitter.com/GITXvCvI2f

— Michael McDonough (@M_McDonough) August 22, 2023

Wondering how US households are coping with 23y high in mortgage rates… well they really are not… yet! Only homebuyers are… Chart shows average effective rate on US mortgage debt outstanding against the spot 30y jumbo rate #fintwit #investing #Economics pic.twitter.com/T1lt7XLI2C

— Philip Jagd (@PhilipJagd) August 22, 2023

Our MORTGAS index (mortgage rates + gas prices) is rapidly approaching 12, hasn't been there since 1990. This was in the 5s back in late 2020. pic.twitter.com/nFPKLhVOJq

— Bespoke (@bespokeinvest) August 17, 2023

U.S. Leading Economic Indicators a bit better year-over-year in July than June.

Manufacturing hours worked a new negative, but stock prices/low jobless claims were positives.

The @Conferenceboard "now forecasts a short and shallow recession Q4 2023 to Q1 2024.” @FactSet pic.twitter.com/Y6rzHN28na

— Matthew Miskin, CFA (@matthew_miskin) August 17, 2023

Leading Economic Index (LEI) from @Conferenceboard declined in July, which marked 16th consecutive contraction … streak that long has only been seen in recessions that started in 1973 and 2007 pic.twitter.com/ThjCW8yQy5

— Liz Ann Sonders (@LizAnnSonders) August 18, 2023

The @NAHBhome housing sentiment print this morning rolling over to 50 is eerily similar to what @MichaelKantro has been highlighting for months around economic cycles (chart below).

The #Fed pivot "house" party may be running out of steam here. pic.twitter.com/IWgkxbY1ev

— Matthew Miskin, CFA (@matthew_miskin) August 15, 2023

Imo, this remains the single most important chart to understand the current macro backdrop.

Bond pessimism vs Equity optimism. https://t.co/EKNH6RU6CD

— Warren Pies (@WarrenPies) August 18, 2023

APOLLO: For the past three quarters, more companies have been downgraded than upgraded — and the higher cost of capital "will continue to create problems for more and more companies characterized by high leverage and low earnings"https://t.co/WbVkNTjwHa pic.twitter.com/nJoeNj2zXV

— Sonali Basak (@sonalibasak) August 15, 2023

Q2 earnings season is in the bag, and it was good: 80% of companies beat estimates by an average of 7.45%. But there has been only a modest bounce in growth estimates (from -9% to -7%). Maybe because Q2 was less of a bullish surprise than Q1. pic.twitter.com/geDnCNdRg9

— Jurrien Timmer (@TimmerFidelity) August 15, 2023

Earnings are backstopping equity markets contrary to all the macro fear. Our BI Global Bellwether group — excluding the commodity-sensitive energy and materials sectors — grew income 6.9% in 2Q, a remarkable gain versus the 0.7% decline anticipated by consensus. pic.twitter.com/KTZ8PAYWFz

— Gina Martin Adams (@GinaMartinAdams) August 15, 2023

The S&P 500 equity risk premium–or diff between earnings yield and 10-year Treasury yield–recently touched the lowest level since **2003**@WSJmarkets pic.twitter.com/M7q1hgr26d

— Gunjan Banerji (@GunjanJS) August 15, 2023

The gift from China that keeps on giving, says @yardeni.

“.. Chinese exporters benefited greatly from the goods buying binge in the US. But they’ve been forced to lower their export prices .. reducing the risks that the US must fall into a recession to bring down inflation.” pic.twitter.com/SD637xcsXh

— Carl Quintanilla (@carlquintanilla) August 15, 2023

Disclosure

Clear Rock Advisors, LLC is registered with the SEC as a registered investment advisor with offices in Texas. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Clear Rock Advisors, LLC) or any investment-related or financial planning consulting services will be profitable, equal any corresponding indicated historical performance level(s), or prove successful. It remains the client’s responsibility to advise Clear Rock Advisors, LLC, in writing, if there are any changes in the client’s personal/financial situation or investment objectives for the purpose of reviewing, evaluating or revising Clear Rock Advisors, LLC’s previous recommendations and/or services, or if the client would like to impose, add to, or modify any reasonable restrictions to Clear Rock Advisors, LLC’s services. A copy of Clear Rock Advisors, LLC’s current written disclosure statement discussing its advisory services and fees are available upon request.