January 31, 2023

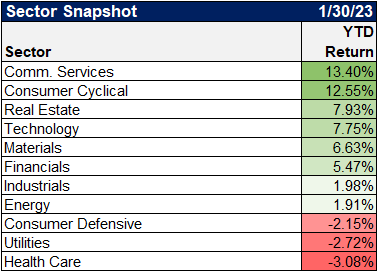

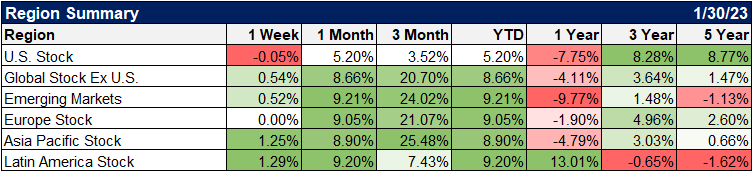

Market Performance (YTD)

Source: YCharts

Disclaimer: Past performance is no guarantee of future performance

Strong headline GDP: 2.9% (ar) in Q4. Led by consumption (+2.1%) but also more volatile factors like inventory investment, net exports and government spending. Residential investment continued its plunge.

Overall GDP basically at CBO's pre-pandemic forecast. pic.twitter.com/tlNDhxtLD8

— Jason Furman (@jasonfurman) January 26, 2023

Real Final Sales to Private Domestic Purchasers is an indicator to watch—it's a mouthful, but essentially represents the "core" of Real US GDP growth (specifically, it's consumption + investment, excluding government spending and net exports).

It's been especially weak recently pic.twitter.com/kkb6sak3KW

— Joey Politano 🏳️🌈 (@JosephPolitano) January 26, 2023

The core PCE index rose 0.3% last month, lowering the 12-month inflation rate to 4.4% (vs. 4.7% in Nov and 5.1% in Oct)

+2.9% at a three-month annualized rate (the lowest since Jan '21)

+3.7% at a six-month annualized rate (the lowest since Mar '21)https://t.co/aqolhkuvrB pic.twitter.com/kZ31xyR0yi

— Nick Timiraos (@NickTimiraos) January 27, 2023

Consumer spending has been the engine keeping the economy moving forward over the past year. So it's a big deal that it fell in December. November also revised down from a small increase to a small decline. pic.twitter.com/XiNF4Y8Yic

— Ben Casselman (@bencasselman) January 27, 2023

🇺🇸Employment Cost Index (ECI) Q4

▶️Still hot, but cooling🟢ECI moderate +1.0% q/q

▶️Wage and salaries +1.0%

▶️Benefits +0.8%🟢All-important private-sector wages & salaries moderate +1.0% q/q

🔥ECI +5.05% y/y (+0.02pt)

🔥Private wages +5.1% y/y (-0.12pt) pic.twitter.com/Dn0az7QSaJ— Gregory Daco (@GregDaco) January 31, 2023

When the Fed hikes rates 25 bps next week, the Fed Funds Rate will move above Core PCE (the Fed's preferred measure of inflation) for the first time since 2019. pic.twitter.com/ALk5YY6Kdw

— Charlie Bilello (@charliebilello) January 27, 2023

Financial conditions have eased significantly over the last three months. In the last 20 years, the only two periods of time where conditions loosened further were toward the end of the 2008-09 recession & mid-2020. pic.twitter.com/OdyJ4PVVBl

— Liz Young (@LizYoungStrat) January 27, 2023

Wild chart from RH/MF at GS.

EPS misses are being bought so far this earnings season in a historic way with stocks outperforming 140 bps after a miss.

This is an all-time best performance dating back to 2006 – stocks have literally never outperformed before on EPS misses. pic.twitter.com/uPq8QOyWeV

— Gavin Baker (@GavinSBaker) January 27, 2023

GDP is nice, but EPS is the primary driver of stock prices.

The chart measures the relative number of earnings downgrades for US stocks versus global stocks over the past 100 days. pic.twitter.com/bQqngENONx

— Jeffrey Kleintop (@JeffreyKleintop) January 28, 2023

Economic surprise improves in Europe, worsens in US.

The problem is that improvement comes from very weak levels.

Shows how poor the macro picture is.

Graph vía Deutsche pic.twitter.com/jVwpPFZhKs

— Daniel Lacalle (@dlacalle_IA) January 24, 2023

The situation in European energy markets is a MAJOR positive surprise to most forecasters

A couple of points on this important topic

First, spot Natural Gas prices are now WELL BELOW THE LEVELS SEEN BEFORE THE RUSSIAN INVASION ON FEB 24, 2022 pic.twitter.com/9yLj9SoBSs

— Jens Nordvig 🇩🇰🇺🇸🇺🇦 (@jnordvig) January 27, 2023

Big positive 2023 real GDP growth revisions last 2 months in China and Europe pic.twitter.com/5pCrRiO33h

— Mike Zaccardi, CFA, CMT (@MikeZaccardi) January 24, 2023

I am starting to sound like a broken record here, but tech sector earnings struggles are still not adequately priced. Tech carries a 23.9% premium vs. the broader index; excluding Microsoft and Apple, it's 18.2%. pic.twitter.com/HyA6p4g1NH

— Gina Martin Adams (@GinaMartinAdams) January 25, 2023

Canada just paused their rate hiking cycle, with an inflation rate and path very similar to that of the US: pic.twitter.com/ycGfFY6y31

— Nick Reece (@nicholastreece) January 25, 2023

Disclosure

Clear Rock Advisors, LLC is registered with the SEC as a registered investment advisor with offices in Texas. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Clear Rock Advisors, LLC) or any investment-related or financial planning consulting services will be profitable, equal any corresponding indicated historical performance level(s), or prove successful. It remains the client’s responsibility to advise Clear Rock Advisors, LLC, in writing, if there are any changes in the client’s personal/financial situation or investment objectives for the purpose of reviewing, evaluating or revising Clear Rock Advisors, LLC’s previous recommendations and/or services, or if the client would like to impose, add to, or modify any reasonable restrictions to Clear Rock Advisors, LLC’s services. A copy of Clear Rock Advisors, LLC’s current written disclosure statement discussing its advisory services and fees are available upon request.