Advantage: US Small Caps

Small cap stocks surged post-election after largely disappointing investors since the financial crisis nine years ago. The historical average small company return premium of about 2% per year above large companies was starting to look like a faded anomaly. Through June of 2016, small stocks underperformed large stocks by almost -5% per year for the previous 3 years. The slow growth QE-driven global economy seemed to favor large and mega cap multi nationals at the expense of more domestically oriented small companies. Those trends have now reversed with small companies significantly outpacing large since the election. What is driving this changing mindset?

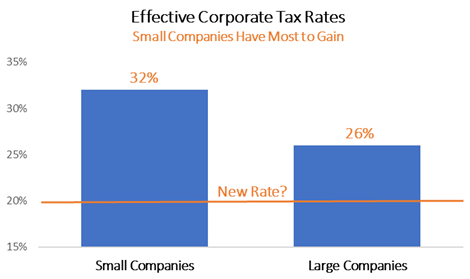

Tax Rates

A lower corporate tax rate is the most obvious benefit small companies have over large. While the same corporate rate applies to all US corporations, small companies generally lack the legal resources and global reach to “hide earnings” from taxation like large companies do. As a result, the effective tax rate paid by small companies is roughly 32% versus large companies who pay and effective rate of 26%.

So large companies currently have a 6% tax rate advantage which drops straight to the bottom line. But who will get the biggest benefit if rates are lowered to a level closer to 20%? Clearly small companies will get the biggest boost – potentially seeing their tax rate drop by 1/3! Shockingly, there are economists and market pundits downplaying this impact that market participants figured out almost instantly.

So large companies currently have a 6% tax rate advantage which drops straight to the bottom line. But who will get the biggest benefit if rates are lowered to a level closer to 20%? Clearly small companies will get the biggest boost – potentially seeing their tax rate drop by 1/3! Shockingly, there are economists and market pundits downplaying this impact that market participants figured out almost instantly.

De-Regulation

Reducing unnecessary and burdensome costs of doing business is seen as a catalyst for job growth by the Trump Administration. Small companies are poised to benefit from these changes more so than large companies. The cost of regulatory compliance is far more onerous for small companies and any relief will be welcomed.

Domestic focus as US growth accelerates

Foreign revenue for small companies averages only 19% of the total – less than half that of large companies whose foreign revenues comprise 45%. If the U.S. sees acceleration in its grow versus the rest of the developed world, companies with more exposure at home should see a relative earnings boost.

Lower debt levels

Small companies have about half the debt load of larger companies. This makes sense given higher risk businesses that are afforded less credit availability. However, the artificially low interest rate environment we’ve been in for the past nine years has favored large companies. As interest rates increase, large companies will be more negatively impacted, which is another relative advantage for small companies.

Higher capex

It is widely believed that large companies have underinvested in their businesses over the past few years, using cash flows and debt financing for things like stock buy backs and dividend increases instead. This is not the case for small companies however, who have continued to invest capital in plant and equipment that make earnings growth from here more sustainable. With the potential for better economic growth, small companies should begin to reap higher rewards on those investments.

Cheaper relative to history

The small company return premium is a function of higher earnings growth rates long term. Historically, investors have been willing to pay up for the opportunity to participate in higher growth, but today, a valuation premium does not exist, even after recent relative outperformance of small companies. Small companies trade at a historically large discount – 25% – to large companies on a price-to-sales basis. That discount is likely to disappear as small company profit margins rise.

Exposure to pro-inflation sectors

As a group, small companies are over-represented in sectors such as financials, industrials and commodities that tend to perform better in inflationary environments. This is a relative advantage to large companies that have higher exposures to slow growth and interest rate sensitive sectors like consumer staples and utilities that have a tougher time passing on inflation through price increases.

Conclusion

Small companies carry higher risk than large companies which can add to the pain of a market correction or economic recession. However, we believe there is still upside from here which underpins our overweight to category within our client equity allocations.

Royce W. Medlin, CFA, CAIA

CIO, Clear Rock Advisors, LLC

www.clearrockadvisors.com