Market Commentary

Q1 2018

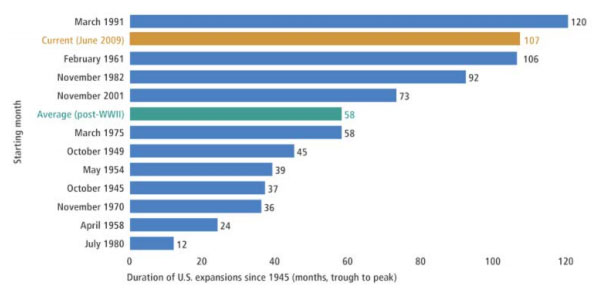

Early or Late Cycle?

There has been a great deal of debate recently over where we are in the business cycle given the recent acceleration of economic growth. Does this expansion’s anemic growth (slowest on record) mean we have avoided the tendency to “overheat”? If so, what is the likelihood of breaking the previous record set in the 1990’s? Our belief is that the economy will continue to do well this year, and perhaps next, which would rank it above all others in longevity (see graph below). The aggressive fiscal stimulus (lower tax rates, higher spending, and increased borrowing) has historically been an early cycle tool while monetary tightening is clearly a late cycle occurrence, so there are mixed signals. However, cycles are inevitable, and a slowdown is likely in 2019 or 2020 when the initial bump from fiscal stimulus fades and the world’s largest central banks move to synchronized quantitative tightening. Eroding slack in labor markets and utilization rates as well as massive re-leveraging by governments, corporations, and households, make it clear that we are in the late, not early, stages of the cycle. However, we continue to believe that a likelihood of a recession this year is low.

Market Jitters

Markets ended the quarter down slightly but with much higher price volatility than the past couple of years. Last quarter, we described 2017 as one of the least volatile markets in history but also warned that Fed tightening cycles tend to bring more volatility which has come to fruition this year. Adding to market concerns are proposed protectionist measures, which are arguably more “fair”, but also recall a difficult period of time for stock returns (1930’s) when protectionism ruled the day. Despite all the rhetoric producing market jitters, economic growth around the globe continues to be strong with an improving outlook for earnings both here and abroad.

Valuation Less of a Concern

A recurring topic of concern is high stock market valuations, particularly in the U.S. Interestingly, valuation risk actually declined over the past few months as higher expected earnings (primarily a result of corporate tax cuts) and a -10% stock correction brought the forward P/E ratio on the S&P 500 down from 18.5x to 16.5x, a level which is closer to the median 30-year P/E of 15x. P/Es in Europe, Japan and Emerging Markets of 14.3x, 13.4x and 12.2x look even more attractive and are also supported by improving fundamentals. 2018 earnings growth in both the US and Emerging Markets is expected to be above 20% with Europe and Japan also expected to generate strong growth this year.

Importance of True Diversification

As we enter into what is likely to be a prolonged period of higher market volatility, the true level of diversification in a portfolio will reveal itself. Many investors have a “diversified” portfolio of stocks that in reality, are 90%+ correlated to each other and not truly diversified. At the same time, bonds have historically served as an offset to stocks but are now challenged by low yields and headwinds as interest rates rise. At Clear Rock, we have scoured the investment universe for strategies that will not only generate attractive returns but provide true portfolio diversification. We look for managers and strategies with the most attractive risk/reward ratios, who are less correlated to traditional stocks and bonds, and will protect capital in a bear market. A compelling example of adding true diversification to our client portfolios is managed futures. Although the strategy has lagged equities lately, it has a history of strong positive performance during equity crisis periods. Each of the 10 worst performing quarters for stocks going back to January 1990 saw positive results for managed futures. During these periods, the average return for managed futures was 5.9%, with only three negative quarters. This compares to the average return of -13.3% for the S&P 500. Importantly, during the worst quarter of the Financial Crisis – the 4th quarter of 2008 – the S&P 500 was down -21.9% compared to a positive 12.7% for managed futures.

1st Quarter 2018 Performance

Stocks

- Stocks globally were down (↓-0.92%). Outperforming were International Emerging (↑1.38%), International Small Cap (↑0.34%) and US Small Cap (↑0.55%). International Developed (↓4.17%), US Large Cap (↓0.76%), US Mid Cap (↓0.77%) lagged. Value stocks underperformed growth stocks by -4.28% during the quarter.

- Looking ahead, global earnings reports continue to be strong, particularly in the US due to tax cuts, which should support stocks through year-end, despite higher volatility.

Bonds

- Broad market bonds sold off (↓1.46%) as interest rates rose during the quarter. Clear Rock bonds outperformed with Investment Grade (↓0.44%), Bank Loans (↑1.39%), High Yield (↑0.28%) primarily as a result of low interest rate risk (duration) exposure. Emerging markets sovereign bonds (↓1.26%) performed worst for the quarter but are the best performing bond investment over a trailing 2-year period.

- Looking forward, bond returns may get a reprieve from higher interest rates in the short term but are unlikely to earn much more than their coupon in 2018.

Alternatives

- The Alternatives portfolio, similar to stocks and bonds, turned in slightly negative performance for the quarter (↓0.75%). All four components were down: Hedged Equity (↓0.86%), Market Neutral (↓0.54%), Managed Futures (↓4.38%) and Multi Alternatives (↓0.23%).

- Despite the lackluster returns for the quarter, we continue to believe in the importance diversification while adding differentiated sources of return with equity-like upside and bond-like risk.

![]()

Royce W. Medlin, CFA, CAIA

Chief Investment Officer