MARKET BRIEF

Bond Returns: Where do we go from here?

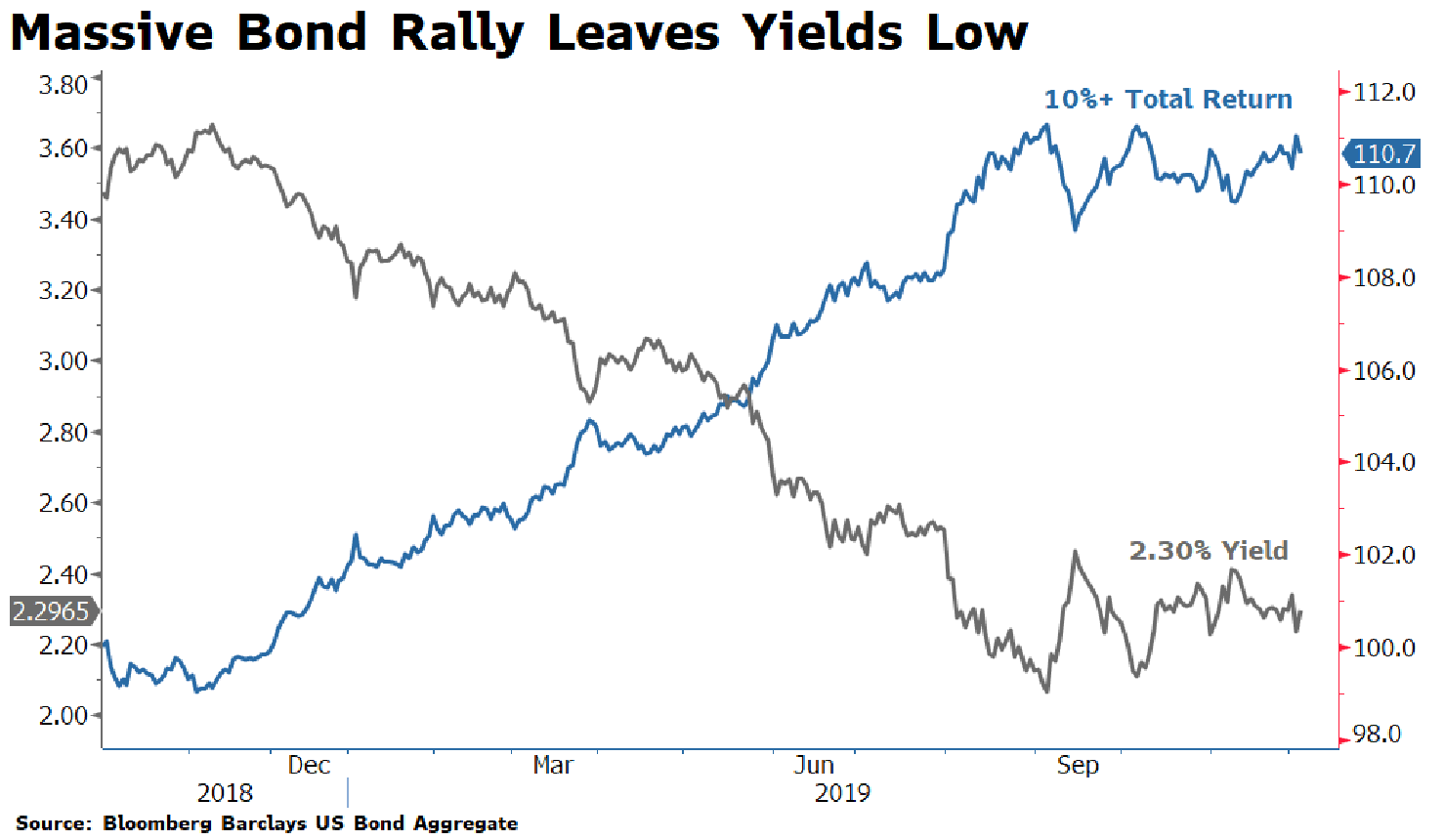

This year’s bond market rally has been one for the record books. A reversal in Fed policy and market fears of a slowing economy produced sharp declines in interest rates. High quality bonds as measured by the US Bond Aggregate (blue line) have produced a 10%+ return over the past year, higher than almost anyone expected and mostly a function of bond price appreciation rather than return from coupon payments. Yields on high quality bonds are back down near all-time lows having fallen from an attractive 3.60% a little over a year ago to 2.30% today (gray line), a -36% decline. This is bad news for savers who are back to earning yields on safe bonds that are barely sufficient to cover inflation.

This low yield on the US Aggregate Index (representing $23 trillion in bonds) now comes with interest rate risk that is the highest on record, having increased 50% over the past 10 years (duration has increased from roughly 4.0 to 6.0 bringing higher bond price sensitivity to changes in interest rates). High duration added rocket fuel to bond returns in 2019 as rates fell – but can also be a headwind when rates rise. Higher rates in 2018 produced a zero total return on the US Aggregate, exacerbated by higher duration as rates rose.

Retail investors have noticed this year’s strong bond market returns and are plowing in new money hoping the momentum will continue. Unfortunately, they are likely to be disappointed. To repeat the rally over the next year, interest rates would have to fall in a similar magnitude. In fact, to achieve a 10% total return on a 10-year US Treasury, yields would have to drop from the relatively low 1.80% today down to 0.82%, a -54% drop, and a level never touched before. The only scenario imaginable that could produce a repeat performance is if the economy moves into a deep recession, which we do not expect. A more likely scenario is that yields remain in a tight range and bond returns reflect their coupon payments of 2.00-2.50% per year.

Low quality bonds (High Yield Corporates and Bank Loans) are likely to produce sub-par performance as well. While yields are higher on average (roughly 5.50%), the premium demanded by investors to lend to riskier companies has shrunk to a level that has little room for improvement. If the economy does slow and corporate default rates increase, there will be downward pricing pressure on these bonds. Over the past year, the stars aligned for low quality bonds with a combination of lower rates, tighter spreads and low default rates pushing up prices to what now appear to be unsustainable levels.

The Clear Rock approach to managing Fixed Income portfolios is to buy bonds when yields are relatively high (as they were last year) and hold off on new purchases when they are low (as they are now). We also enhance returns through selective allocation to higher risk sectors such as High Yield, Bank Loans, Emerging Markets Debt, and Securitized Credit, but only when the risk/reward is highly attractive.

Due to rapidly increasing debt loads by US corporations, we eliminated our exposure to the High Yield and Bank Loan sectors last year and reallocated into Securitized Credit (mostly high-quality mortgage-backed securities).

Slowing growth in emerging markets convinced us to remove exposure to this sector almost two years ago. However, many developing countries have seen recent improvements in their growth rates as fiscal and monetary stimulus has taken hold. This has increased credit quality and made the sector more attractive for potential future investment.

Finally, US household debt burdens have shrunken dramatically relative to the highs reached during the last recession and accelerating real wage growth further improved balance sheets. As a result, we believe mortgage-backed securities are attractive on a risk/reward basis, particularly compared to lower quality corporate bonds and loans where we believe debt ratios are dangerously high.

2019 has been an interesting year, marked by the Fed’s about-face on monetary policy. Moving from doggedly hawkish in 2018 – raising interest rates and removing liquidity from the economy – to wildly dovish in 2019 – implementing three quick rate cuts and reintroducing quantitative easing. Market moves in both years seemed to reflect the old saying, “Don’t Fight the Fed”. The impact of these moves longer term are yet to be determined but a repeat of the bond rally is highly unlikely.

Respectfully,

![]()

Royce W. Medlin, CFA, CAIA

Chief Investment Officer