How to Find Defense & Yield at The Same Time

It’s hard to say if now is the time to play defense in the markets. On one hand, we have trillions of dollars in stimulus still making its rounds, vaccines being distributed at a faster pace across the globe, and financially healthy consumers. It’s hard to imagine a scenario where the market freefalls during a time of historical economic expansion. But on the other hand, the S&P 500 is now trading at the highest price-to-sales ever. By most historical metrics, equity valuations are stretched, and it feels like the expectation of a historical economic boom is already baked into the economy. But when was the last time we experienced a stock market crash during an economic boom? There’s no easy answer here, but let’s say you wanted to play defense—where would you invest? The typical answer is fixed income, but there’s an argument to be made that the fixed income market is just as stretched, if not more, than the equity market. Roughly 80% of investment grade corporate debt is trading at less than 1%. There is currently ~15 trillion in negative yielding debt. High yield bond spreads just hit lows not seen since 2007 and are only yielding around 4%. CCC rated bonds are at all time low yields. It’s a tough environment for a conservative investor, especially those looking for yield.

We believe investors can not only enter attractive parts of the market, but also find attractive yields and play a little defense in two areas that fall into a category that we call ‘less liquid alternatives.’

Private Real Estate

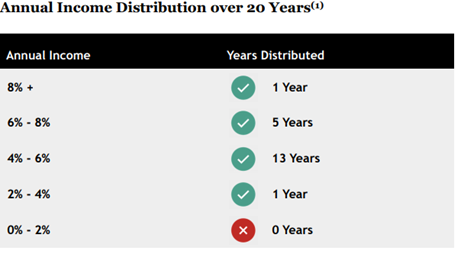

The first is private real estate. The private real estate market is not immune to the stretched nature of the public equity and fixed income market, but it offers an attractive risk-reward, comparatively speaking. The reward is typically higher yields, as the accompanying chart from Blackstone shows, with less volatility due to the private structure. The private structure is an advantage, primarily mentally, during short periods of stress like we saw in March 2020. This is an important advantage as market sell-offs and rebounds continue to just get quicker and swifter as markets progress in sophistication.

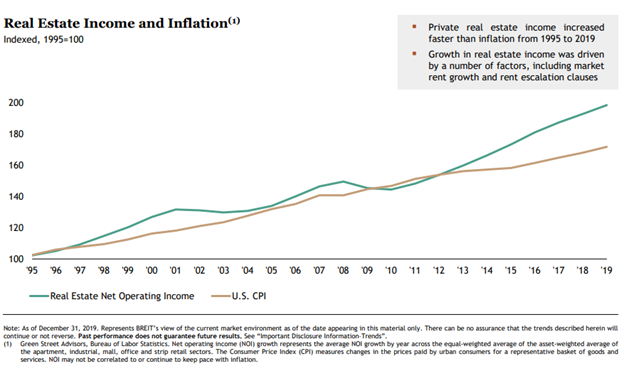

In addition to the high yield and private structure, private real estate is positioned well in the market. The spread between real estate cap rates and interest rates remains high, creating an opportunity not currently available in the public markets. Plus, for the first time in over a year, the biggest risk to investors is not coronavirus—it’s inflation. We aren’t overly concerned about inflation, but it is a risk, and the real estate market is a good place to hedge this risk. The accompanying chart from Blackstone shows why real estate has typically been a good place to be during inflationary times—rent income typically increases faster than the rate of inflation.

Private Credit

The second is private credit. Private credit, in its purest form, is similar to the public high yield market. But instead of being a collection of public loans/bonds/credit instruments, it’s a collection of privately negotiated loans/bonds/credit instruments.

From a risk perspective, private credit is attractive when compared to the high yield market. First and foremost, managers in private credit can negotiate their portfolio of loans, both from an individual loan and total portfolio perspective. In their credit analysis, they can select the deals they want, and can negotiate the covenants, collateral, and seniorities they want. This process results in private credit typically having higher seniority, more call protection, and better covenants. Private credit is typically secured; 1st lien, unitranche, and 2nd lien debt, whereas high yield is typically unsecured; subordinated debt. Because of the due diligence process, private credit typically has better credit ratings, and because private credit is a collection of privately held loans instead of publicly held loans, private credit is typically much less sector concentrated. Almost half of the high yield index is in the energy and consumer sectors, whereas most private credit managers keep their portfolios very diversified.

This ability to negotiate loan terms has proven beneficial for investors. Over the past fifteen years, private credit has earned 9.2% while the high yield index earned 7.1%, according to Blackstone. More importantly, private credit is positioned better for the future. Private credit is typically made up of floating rate loans while high yield is typically made up of fixed rate loans. The floating rate structure allows private credit funds to benefit from a rising rate environment because rising rates mean higher coupons and thus higher distributions. This structure is advantageous when compared to a fixed rate structure in a rising rate environment because coupons don’t increase in a rising rate environment for fixed rate loans, like they do for floating rate loans, while the price for fixed rate loans decreases, thus the value of the loans decreases, exactly the opposite to what happens for floating rate loans.

Higher Fees, Less Liquidity but Worth It

Though ultimately beneficial, the private structure of these two areas does create hurdles and have risks. The biggest risk—one for which you are paid a premium for—is liquidity risk. Many of these structures only allow for quarterly or monthly liquidity, hindering some people’s ability to invest. Plus, because these funds are privately negotiated and managed, fees are higher. At the end of the day, though, net returns are what matter—and we believe the net returns going forward will still prove attractive when compared their public market peers.

On a quarterly call recently, one of the managers said, “You don’t make money with 100 basis points of yield, you make money in credit by not losing it.” Typically, these types of funds harp on risk management, and, for the most part, they have proven they manage risk better than their public market peers, largely because the public market in these areas are rife with problems, the private structure eases volatility, and the managers can analyze and manage their credits. They can do all of this while demanding higher yields—that’s why they are worth the fees.

From a portfolio perspective, private real estate makes sense because it’s relatively stable and has proven to be a good inflation hedge over time. Private credit also makes sense because of its low correlation to investment grade bonds; it’s relatively low volatility; and its ability to earn higher returns during a rising rate environment. Not to mention these both offer high yields. We believe these ‘less liquid’ alternatives deserve an allocation in a portfolio, if one can swallow the liquidity risk and higher fees, because they allow investors to enter attractive, growing parts of the market, earn a higher yield, and play a little defense all at the same time.