Market Commentary

Q2 2020

“V” Shaped Recovery

The first half of the year felt like an eternity with unprecedented economic and market volatility. The COVID global economic shutdown caused asset prices and economic activity to plummet almost overnight. The S&P 500 fell 34% but quickly bottomed on March 23 and has rebounded strongly since, now down about -2% since the beginning of the year. Despite woeful economic statistics being reported throughout the month of April, the S&P 500 turned in its best one month return since World War II. The rebound was primarily the result of record monetary and fiscal stimulus designed to bridge households and corporations for the reopening of the economy. Optimism also reflected a declining COVID curve, oil price recovery and reopening announcements. Some downside volatility occurred in June based on fear of a COVID second wave, but the market quickly dismissed those fears and resumed its upward trajectory.

While massive stimulus has provided ample liquidity to stressed households and corporations, we worry that a “V” shaped recovery may prove optimistic as emergency spending measures fade. Many furloughed employees have been rehired, but many have not. Generous government benefits for the unemployed expire this month and while they may be extended, a large portion of those out of work are unlikely to return in the near term. We expect Congress to extend relief to the unemployed but also worry that many job seekers will face fewer opportunities than before with new jobs looking much different than they did pre- COVID.

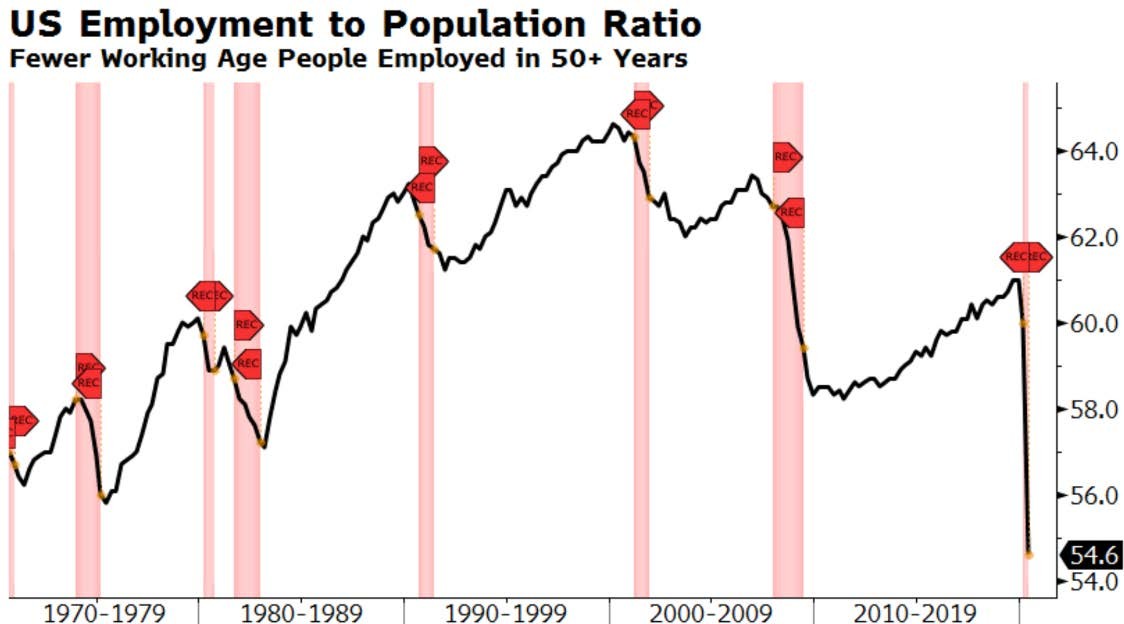

As daunting as the current unemployment rate of 11% is, even more worrisome is the employment-to- population ratio of 54.6% which has dropped to an all- time low (see accompanying chart). Today, a little over half of working age Americans are employed, down from a peak 20 years ago of almost 65%. Millions of jobs need to be created to maintain growth in our economy which is heavily dependent on consumer spending.

The last economic expansion was the longest in history but suffered from low growth, low productivity, and growing debt. While the COVID recession will likely go down in history as the shortest and deepest, it will also be notable for its lack of debt defaults relative to past recessions, despite high corporate debt ratios. Massive debt issuance by corporations over the past couple of months, made possible by aggressive monetary policy, has created financial support and flexibility but also increases the likelihood of a more painful default cycle in the next downturn.

The Post-COVID economic expansion will carry higher debt levels across all sectors – government, corporate and household – that will restrain growth and eventually force taxes higher and confidence lower. Over the next few months, we believe the narrative will change from exuberance around the “V” shaped recovery to concern about the inevitable fiscal spending cliff when stimulus runs out. Fed intervention on the other hand, appears to be unlimited. There is worry however that low interest rates may be less effective than they have in the past at invigorating real economic growth.

Uncertain Fundamentals

Earnings projections since the beginning of the year have dropped by -30%, the worst decline since 2009. While the S&P 500 initially fell in a similar magnitude, it is now only down -2%. Needless to say, an earnings recovery is being discounted into today’s stock prices.

The strength of the S&P 500 is somewhat misleading and masks underlying weakness. This index is heavily weighted toward a handful of mega- cap stocks that have led the recovery while most companies in the index have not fully recovered.

Looking at the price performance of the median US stock tells another story, one that is significantly less bullish and reflects an uncertain outlook. The accompanying chart shows the Valueline Geometric Index which is made up of 1700 US stocks and is equally weighted, giving small and large companies the same weight. This index shows the average US stock still down -20% this year and even worse, down -15% over the past three years. This reflects underperformance of smaller and mid-sized companies that have historically grown faster and been an engine for job growth. The average stock is also much more attractively valued and offers better upside potential long term than the mega cap leaders whose valuations are once again extended.

Portfolio Positioning

In our last quarterly commentary, we highlighted our move from “Protect” to “Normal” strategic allocations across all client investment objectives. This active decision was designed to take advantage of attractive buying opportunities created by the sell-off. The move pushed portfolio weights to stocks and credit strategies higher to take advantage of convincing opportunities for appreciation. Fortunately, those moves paid off. We added significantly and quickly to stocks at oversold levels in early April and participated in the powerful recovery. The source of funds used to boost stocks came primarily from alternatives which outperformed through the sell-off, playing exactly the role in the portfolio we had hoped they would.

2Q 2020 Performance

Stocks

- We began the quarter at an oversold level for stocks and were able to add significantly at lower prices.

- Stocks recorded one of the best quarters in market history. Globally, stocks were up (↑21.62%) with strong gains in US Mid Cap (↑24.06), US Small Cap (↑21.73%), US Large Cap (↑20.16%), International Developed (↑15.35%), and Emerging Markets (↑17.86%).

Bonds

- Opportunities appeared in credit strategies during the sell-off as credit spreads widened to crisis levels and yields became attractive. We took advantage of higher yields through our new investments in High Yield Corporates and Emerging Markets Bonds.

- Yields on high quality bonds remain low with the US Aggregate Bond Index yield at 1.2%. Total return on Municipal Bonds gained slightly during the quarter (↑1.22%), although the average yield on the 10 Year Baseline AAA National Muni is at an all-time low of 0.86%. Securitized Credit recovered strongly (↑11.08%), as did High Yield Corporates (↑8.64%) and Emerging Markets Debt (↑13.95%).

Alternatives

- After holding up well during the 1Q market sell-off, alternatives were up slightly in 2Q, exhibiting very little correlation with the stock market.

- The Alternatives portfolio was up slightly (↑1.17%) for the quarter. Category performance was led by Multi Strategy (↑7.56%) and Market Neutral (↑2.77%). After strong positive performance through the market sell-off, Managed Futures gave back gains (↓4.61%) in 2Q. Real Assets showed positive performance in 1Q during the sell-off but delayed monthly pricing pushed performance for 2Q to (↓6.02%).

As always, contact us if would like to discuss these topics further.

Respectfully,

![]()

Royce W. Medlin, CFA, CAIA

Chief Investment Officer